Budget 2025 was announced on 1st October to much excitement and media coverage and it included a personal income tax package of €1.6 billion. It increased the standard tax rate bands by €2,000, the personal credits by €125 and provided for a 1% reduction in USC on earnings from €27,382 and €70,044.

Last week Minister Chambers followed through with the release of the 2024 Finance Bill in Ireland. The new Finance Bill sets out the legal framework to the budget measures announced. It also provided some much-needed clarity on specific legislative adjustments (and a few surprises!). It is worth noting that the Finance Bill can still undergo amendments as it passes through the houses of the Oireachtas over the next few weeks before being signed into law.

As always, the devil is in the detail, so we have pulled together some Contractor Highlights from this new Finance Bill, that may benefit you.

The Finance Bill has implemented a new limit on the tax relief available for employer contributions to Personal Retirement Savings Accounts (PRSAs) and Pan-European Pension Products (PEPPs). From 1 January 2025, an employee or director will be liable to an income tax charge for any amount paid by the company into their pension that is greater than their salary.

Additionally the company won’t be able to claim a deduction for the amount of pension contribution over the amount of salary.

The Standard Fund Threshold is the maximum limit of your tax-relieved pension fund. From 2026, the Finance Bill increases the SFT on a phased basis by €200,000 per year resulting in a SFT of €2.8 million in 2029. From 2030 the threshold will then be indexed annually by an earnings factor.

Previously known as the much-anticipated Auto Enrolment system, My Future Fund is due to begin on 30 September 2025. This is the new retirement savings scheme for people without a work or private pension. Employees will automatically be enrolled in the scheme once they are aged between 23 and 60, earn more than €20,000 per year, and are not currently paying into a work or private pension through payroll. An individual will have the option to opt-out after 6 months from the date of their automatic enrolment in the scheme.

From 1 January 2025, the tax-exempt limit on small benefit awards for employees was increased from €1,000 to €1,500. This can be granted in up to 5 non-cash benefits in a single tax year. This relief is due to expire in 2030.

The temporary one-year tax credit available has been extended for taxpayers with an outstanding mortgage balance of between €80,000 and €500,000 as of 31 December 2022. This credit can only be claimed on principal private residences (PPR).

For more information, click here.

The Finance Bill confirms the increase to the amount of the Rent Tax Credit from €750 to €1,000, or, in the case of jointly assessed taxpayers the relief is increased from €1,500 to €2,000 for tax years 2024 and 2025. More information click here.

For individuals coming to or leaving Ireland, Split Year Relief is a valuable relief which reduces the tax due in Ireland on foreign employment income in the year of arrival/ departure.

The 2024 Finance Bill provides a welcome change to Split Year Treatment whereby the individual arriving to or departing from Ireland is not required to advise Revenue of their intentions. Rather, they can claim this relief via their Personal Tax Return.

The Finance Bill has provided an extension to the deduction for certain ‘pre-letting’ expenses (up to a max of €10,000 per property), for a further three years to the end of 2027. The deduction is allowed on expenses incurred on a property that has been vacant for at least six months and which is subsequently let as a residential premises on or before 31 December 2027.

The HTB scheme is being extended for a further four years until 31 December 2029.

The scheme will continue to assist first-time buyers with buying or building a new house or apartment by giving a refund of Income Tax and Deposit Interest Retention Tax (DIRT) paid over the previous four years, subject to qualifying criteria.

The Finance Bill has extended the temporary universal reduction of €10,000 applied to the Original Market Value of vehicles in Categories A-D (including vans) and the amendment to the lower limit of the highest mileage band (52,001km to 48,001km) to 31 December 2025.

The Bill also confirmed the Budget Day announcement for an exemption from BIK where a Company incurs an expense in providing a facility for the electric charging of vehicles at the home of a director or an employee.

Additionally, the Finance Bill also includes an exemption from BIK where facilities for the charging of electric vehicles are provided on a business premises where all employees and directors can avail of such facilities. More information click here.

EII is a tax relief which aims to encourage individuals to provide equity-based finance to trading companies.

Currently, the maximum investment on which a taxpayer can claim relief is €500,000 per year of assessment where the EII shares are held for a minimum period of 4 years. From 1 January 2025, this has now been increased to €1,000,000.

SURE is a tax relief that provides a refund of Income Tax that you paid in previous years. You can claim the relief if you are starting your own business and you are an employee, an unemployed person or a person who has recently been made redundant.

The Bill increases the maximum relief available for SURE investments from €100,000 to €140,000 per year.

The R&D Tax Credit is a 30% tax credit for all qualifying R&D expenditure. From 1 January 2025, the first-year payment threshold is increased to €75,000. Previously it was €50,000. This threshold is the amount up to which a claim can be paid in full in the first year, rather than paid in instalments over three years as is usually the case.

The Finance Bill provides an increase to the CGT relief for qualifying investors who acquire between 5%-49% of innovative start-up SME companies. It allows those investors to avail of a reduced rate of CGT of 16% on a gain up to twice the value of their initial investment. An effective reduced rate of 18% applies to individuals who make the investment via a qualifying partnership.

There is a lifetime limit of €10 million on gains that may avail of this reduced rate of CGT.

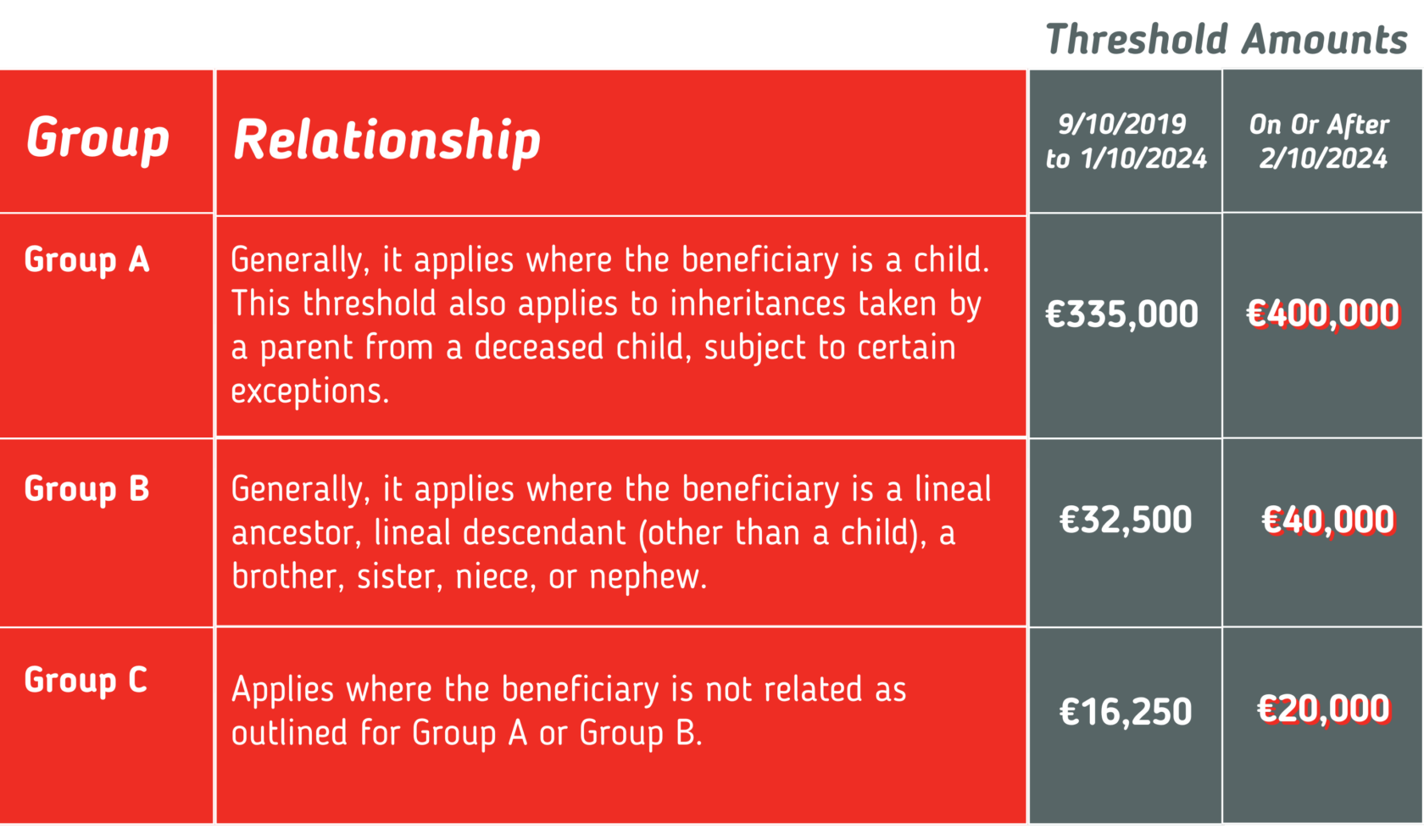

As widely expected, the CAT Group Thresholds were increased as follows:

Additionally, from January 1 2025, all low interest family loans with a value greater than €335,000 must be reported to Revenue.

The Bill provides for some changes to Retirement Relief. From 1 January 2025, CGT relief is only available on disposals to a child valued over €10 million provided the assets are retained for a 12-year period. This would apply in relation to the CGT liability arising in respect of:

Where a clawback occurs, the onus is on the child and not the parent.

This article has been carefully prepared, but it has been written in general terms and should be seen as broad guidance only. Information correct at date of publish 17th October 2024.

Would you like to be redirected to our Indian website?