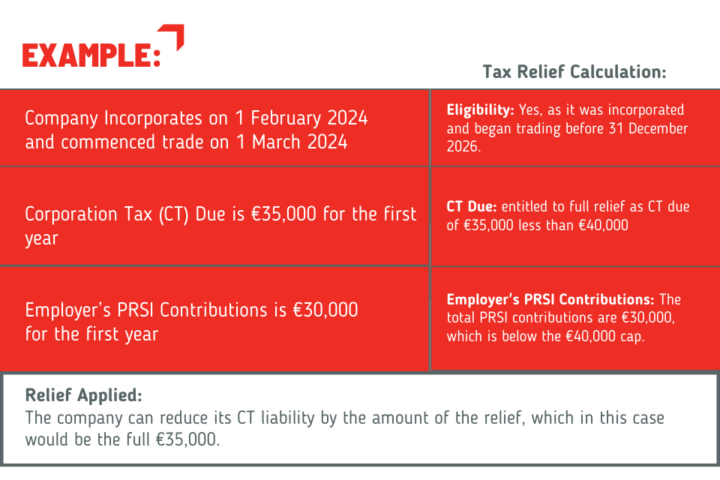

A recent paper from the Department of Finances Tax Strategy group comments on the low uptake of the various supports available, citing that there is a perceived complexity involved.

So, let’s take a simple snapshot of Government Supports available for start-ups and companies…

Our Thoughts

Our ThoughtsThis is a great tax relief for start-up businesses but the relief is not really of any use for independent professionals as companies providing ‘services’ are typically excluded, and most contractors and freelancers typically work on their own and don’t have employees.

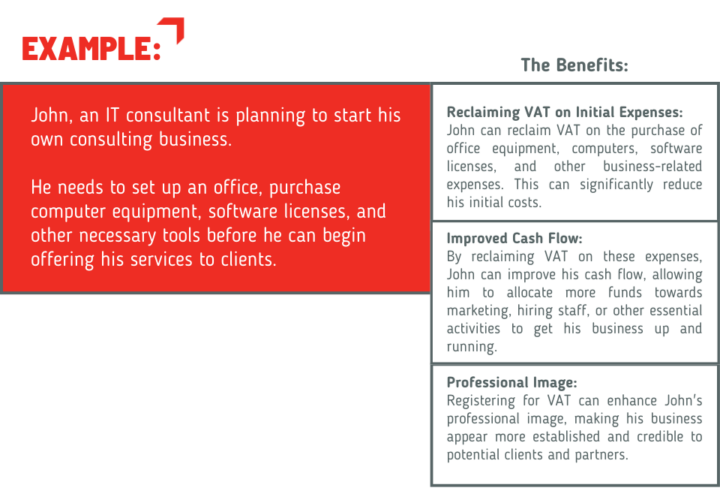

Even if your business has not yet commenced trading, you can register as an intending trader. This allows you to buy stock, equipment, and other necessary items with a view to trading. Registration as an intending trader can help you establish your business and prepare for future operations.

Revenue apply stringent screening and verification processes to ensure only legitimate businesses are granted VAT registration, which can delay the approval process for genuine applicants. Contractors using our services benefit from our expertise and experience in setting them up in VAT registered companies so that there is no delay in claiming VAT back on their expenses.

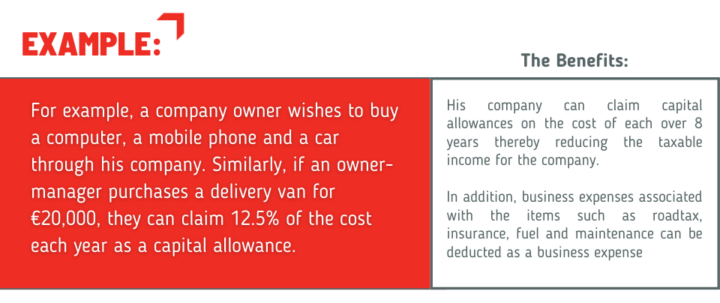

As a self-employed individual, you can claim more deductions than an employee, providing more opportunities to reduce your tax bill. You can also claim capital allowances on certain expenditure, which can significantly benefit your business finances.

Purchasing capital assets through a company offers tax advantages for the company however it also comes with potential benefit in kind taxation for the individual and caution is needed with some assets that the individual might like to own in the future in their own name.

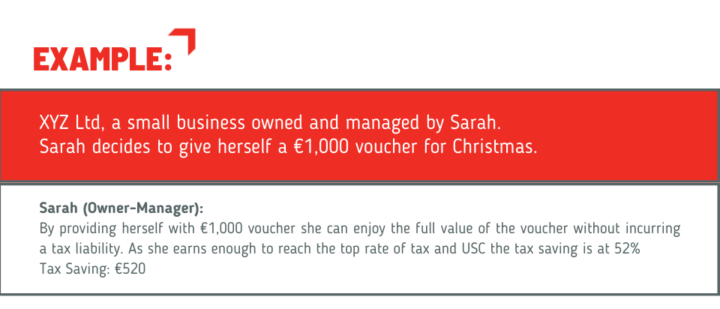

The Small Benefit Exemption scheme allows employers to provide employees with small benefits, such as vouchers, without the benefit being subject to tax, PRSI, or USC, provided certain conditions are met.

This scheme can be particularly advantageous for owners of a small businesses, but note it is not available to sole traders.

The Small Benefit Exemption scheme is a valuable tool for contractors and freelancers, allowing you to buy a €1000 voucher every year through your company and using it on whatever you want to spend it on, be that a holiday, fashion, food shopping….anything you want.

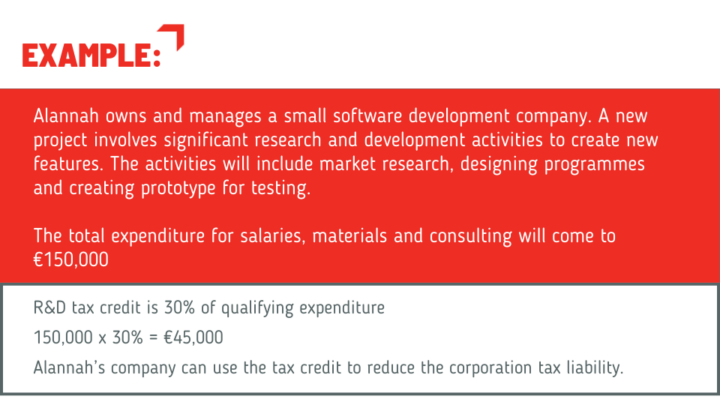

If your company engages in qualifying R&D activities, you may be able to claim a corporation tax credit of 25% of your R&D expenditure. Small and micro companies with fewer than 50 employees and annual turnover below €10 million benefit from a 30% R&D tax credit on qualifying expenditure. This can be a substantial benefit for companies involved in innovative and developmental projects.

The R&D tax credit has several limitations and conditions as detailed records and documentation are required, the process for claiming the credit is lengthy and complex. To maximise the chances of approval it is necessary to understand the criteria, maintain evidentiary materials and make a pre-filing notification to Revenue. It’s a great tax credit for thinking of developing a piece of software or a product.

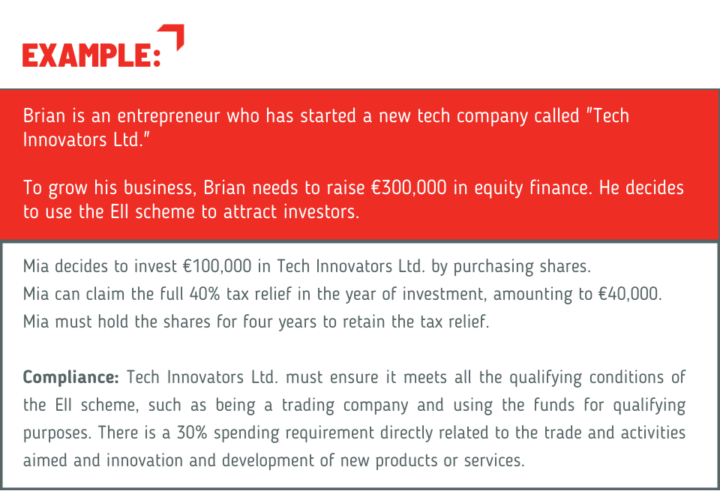

The EII Scheme provides tax relief for investors who purchase new shares in qualifying small and medium-sized enterprises (SMEs). This can be an excellent way to attract investment and grow your business.

The Employment Investment Incentive Scheme (EIIS) presents several challenges. it involves significant paperwork. Companies must file several forms, such as the Return of Qualifying Investments in a Qualifying Company and the Form RICT, electronically with Revenue. Additionally, they must issue a Statement of Qualification (SOQ) to investors within four months after the end of the tax year in which the shares were issued. This administrative burden can be challenging for companies to manage effectively. They need to spend at least 30% of the funds on qualifying purposes, which requires careful financial planning. Additionally, the self-certification process, while reducing administrative burden, carries the risk of incorrect certification, which can lead to a clawback of relief. Finally, the requirement to hold shares for a minimum of four years may deter some investors. This relief is good but not for the faint hearted!

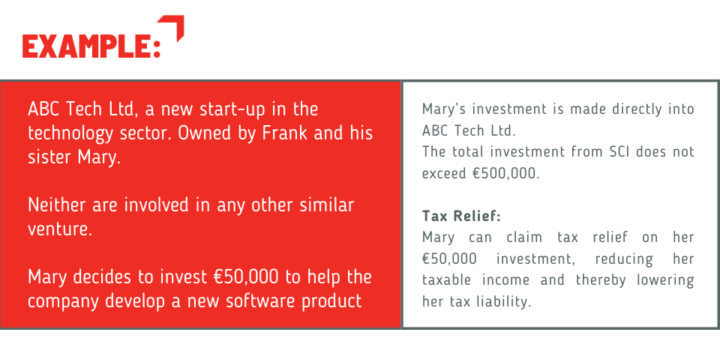

The Start-Up Capital Incentive (SCI) is designed to assist start-up companies in raising equity financing, particularly from family members of existing shareholders. To avail of the relief, the company must be carrying on a new venture, and none of the shareholders can carry on a similar venture. The most a company can raise from SCI investment is €500,000.

While the Start-up Capital Incentive (SCI) provides valuable tax relief and encourages family members to invest in new ventures, it comes with specific eligibility criteria, investment limits, potential clawbacks, administrative requirements, and investment risks.

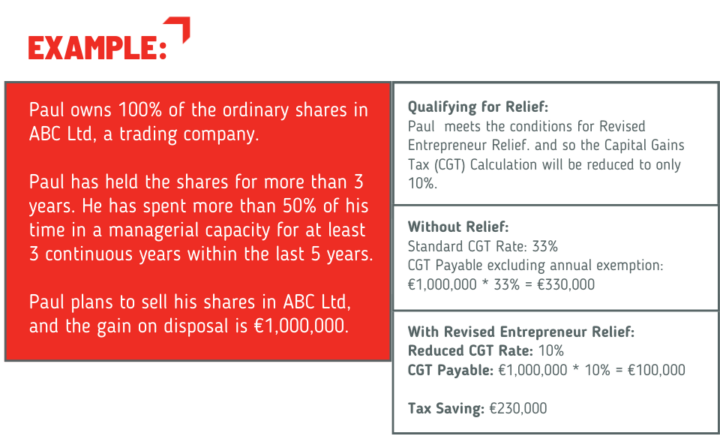

Entrepreneur Relief is a significant support for business owners looking to dispose of their business assets. This relief allows for a reduced Capital Gains Tax (CGT) rate of 10% on gains from qualifying business assets. A qualifying business excludes activities such as holding investment assets.

To qualify, you must have owned at least 5% of the company’s ordinary shares for a continuous period of 3 years at any time prior to disposal. You must have also spent no less than 50% of your time in the service of the company in a managerial or technical capacity for a continuous period of three years within the five years immediately prior to the disposal of the business assets. It has a decent lifetime limit of €1 million.

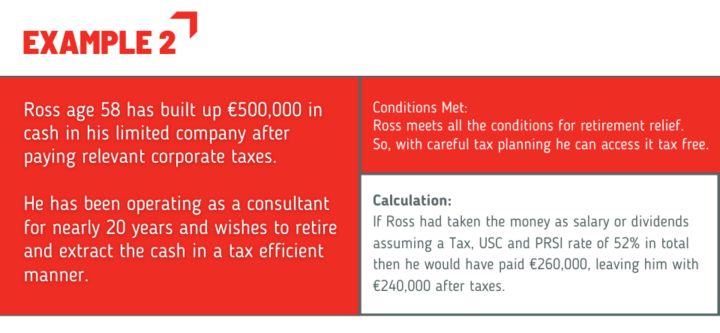

By retaining profits in the company and reinvesting in the business, owners can defer personal income tax which can be as high as 52% (including USC and PRSI) on salary or dividends. They can build up money in a tax-efficient manner and benefit from the Revised Entrepreneur Relief when eventually selling shares or liquidating, resulting in substantial tax savings. That being said there are several limitations including strict conditions, lifetime caps and administration complexity to navigate.

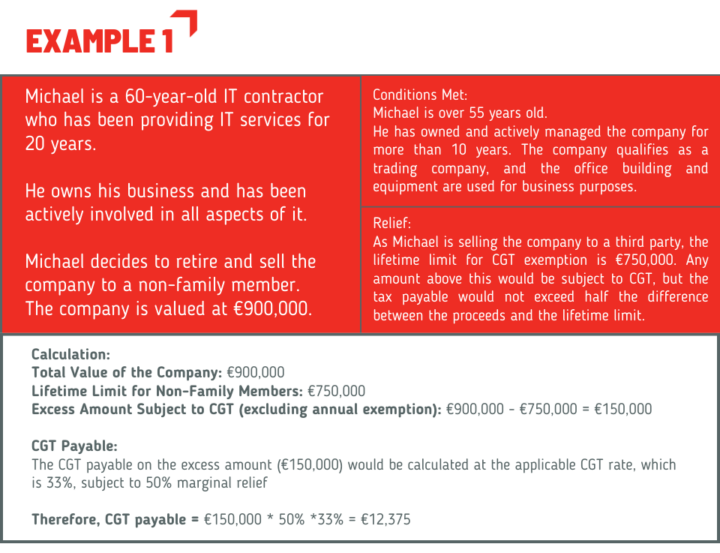

Retirement Relief is a valuable tax relief available to individuals aged 55 or over who dispose of certain business assets. Despite its name, you do not need to retire to avail of this relief. The relief can significantly reduce or eliminate the Capital Gains Tax (CGT) liability on the disposal of qualifying assets, such as a farm, business, or shares in a family company.

Key points to consider include the Lifetime limit and the ownership period and note some changes are being introduced from 1 January 2025.

The ability to save up money in a tax efficient manner in your company should not be overlooked. Pensions remain the most beneficial way of saving tax, but if you’re happy with the growth trajectory of your pension, and you still have surplus cash that you don’t need to live on, then the Retirement relief allowing you take €750k tax free is very attractive.

Navigating the various supports and reliefs available can be complex, but you don’t have to do it alone. Our team of experts is here to guide you through the process, ensuring you make the most of the opportunities available to you. We can help you understand the eligibility criteria, prepare the necessary documentation, and apply for the supports that best suit your business needs.

This article is for information purposes only and you should get professional tax planning specific to your circumstances and what you want to achieve.

Article written on the 16/09/2024

Would you like to be redirected to our Indian website?